A deep evaluation of the present state of automotive and aftermarket gross sales, along with the main traits impacting the trade – from the macroeconomic panorama to customers’ financial pressures, and the newest areas of innovation-led transformation which can be unlocking pockets of progress.

Final yr noticed consumers across the world shopping for 68 million new automobiles, a vital soar in yr–on–yr progress that brings the trade nearer to the pre-pandemic benchmark of 73 million purchased in 2019. For 2024, the common view is that gross sales will attain round 70 million.

This yr’s extra muted progress forecast is on account of a lot of the pent-up demand from the low-production years of 2020-2022 having now principally been glad, together with the continuing financial challenges confronted by customers throughout totally different areas.

For instance, APAC is a high-potential region with very low automobile penetration. Final yr, gross sales of latest automobiles there grew by +9%, based on Statista, however expectation for this yr runs at simply +2%, largely on account of low efficiency forecast for China.

For this yr, then, Europe seems to be the area offering best progress alternatives, adopted by North America – however, even in these two markets, the speed of progress for brand spanking new automobile gross sales is depressed.

-

Second hand automobile gross sales and automotive aftermarket – 2024 alternatives

Globally, we count on to see 36.2 million used automobile gross sales this yr, simply up from 35.9 million in 2023.

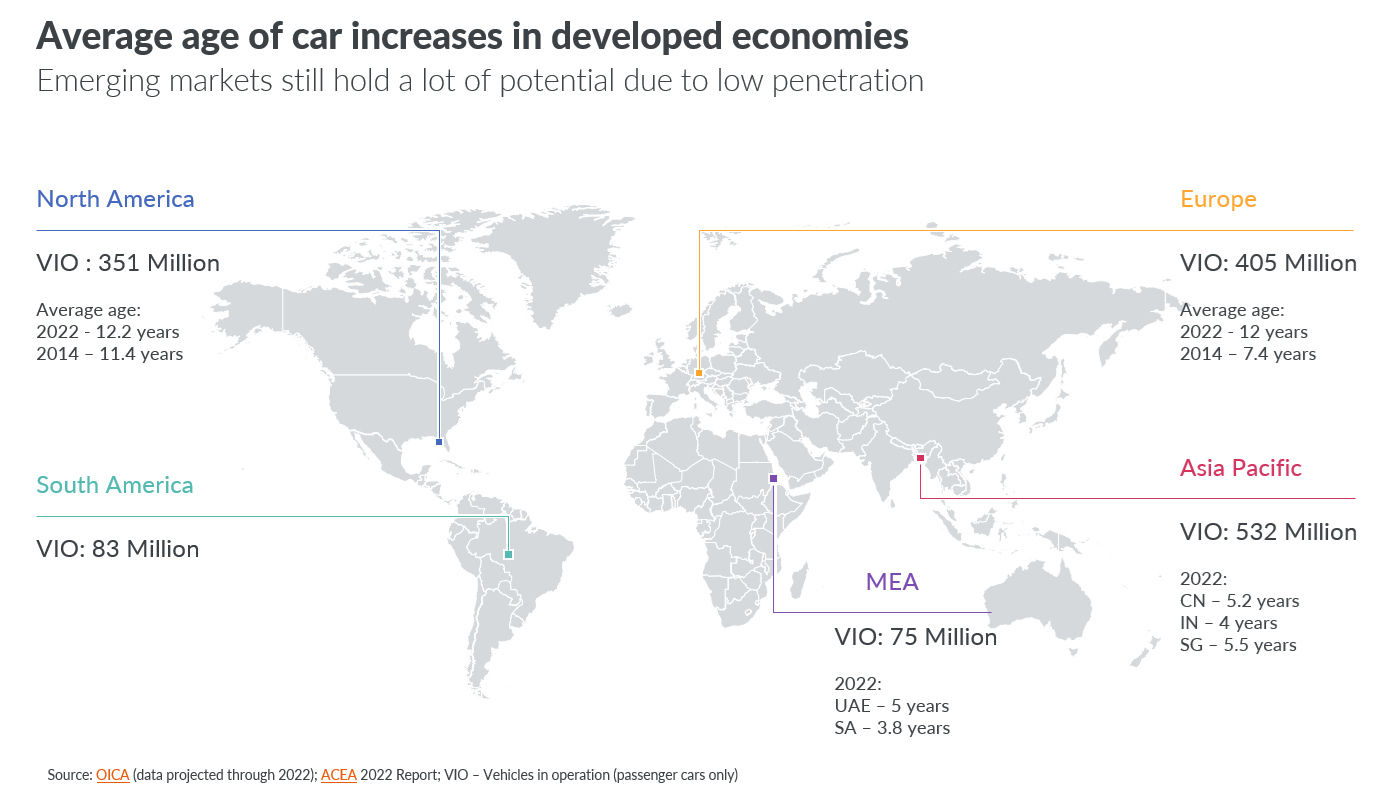

In Europe and North America, the common age of automobiles in operation has elevated from 7.4 years previous (Europe) and 11.4 years previous (USA) ten years in the past to 12 years previous now. That is based on newest knowledge from OICA, the Worldwide Group of Motor Automobile Producers.

With over 750 million passenger automobiles in operation on those two continents, we count on to see rising demand for aftermarket merchandise as the upkeep necessities of these older automobiles grows.

Tempering that potential income pot for aftermarket gross sales, nonetheless, is the truth that, as soon as their automobiles attain 5 or 6 years’ previous, individuals turn out to be much less inclined to splash out on their upkeep, and extra possible to decide on funds–friendly moderately than premium components.

In Asia Pacific and the Center East, we see a special image and set of alternatives. In these areas, the common age of automobiles sits at round 4 to 5 years previous. With a rising center class throughout a lot of these areas, and comparatively low automobile penetration, this currents potential for a spike in new automobile gross sales from customers wishing to improve their lifestyle and show their elevated wealth.

Moreover, the truth that individuals listed below are exchanging their automobiles after solely 4 or 5 years currents opportunity for the second–hand automobile market. Not solely is it in a position to supply youthful, higher high quality automobiles which ought to drive robust gross sales potential, however we count on a increase to after-market gross sales too, as rising middle-class patrons who might not have felt in a position to afford a brand new automobile look to improve their second-hand buy with premium components, tires, and automobile chemical compounds.

-

Automotive aftermarket gross sales displaying continued progress

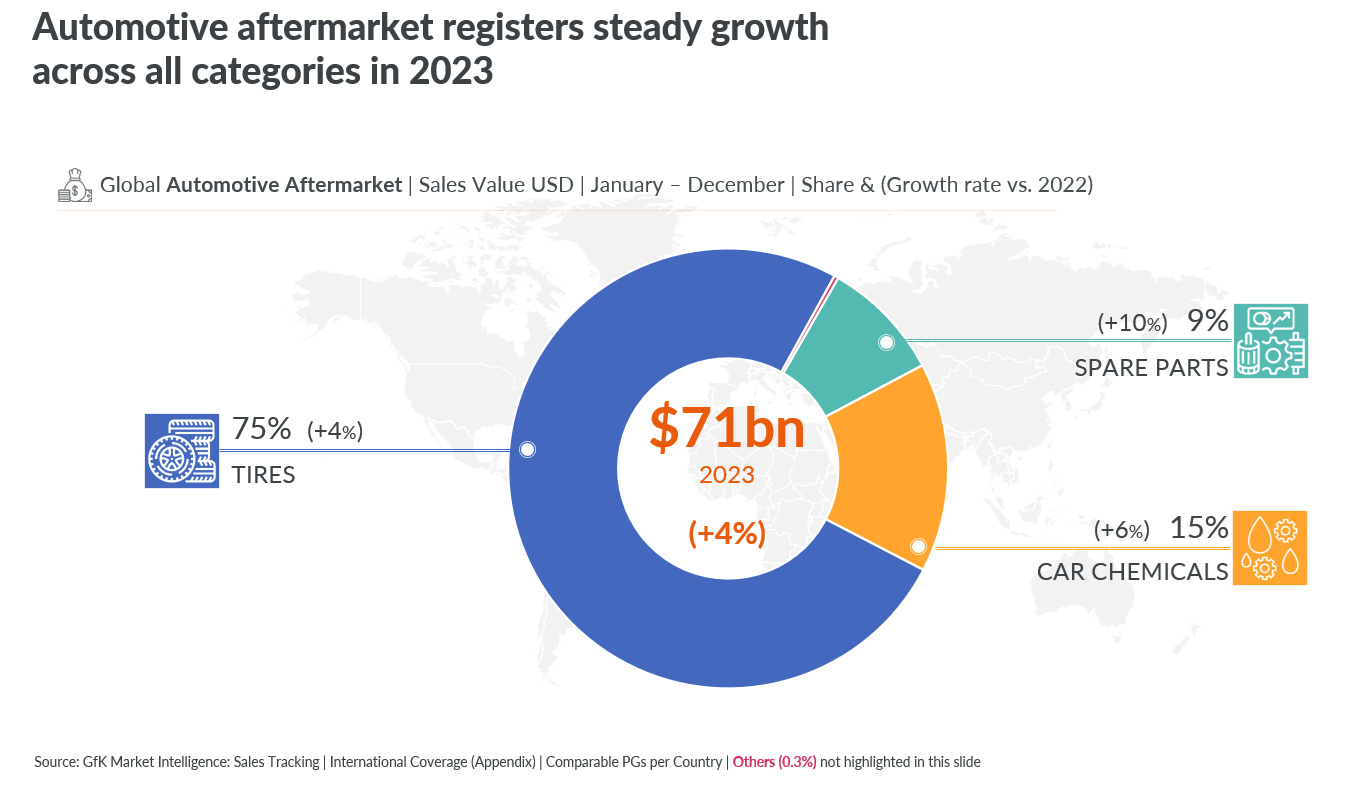

The international automotive aftermarket is continuous to develop with gross sales income up +4% final yr, reaching $71 billion. That is on prime of a +3% progress already seen in 2022 versus 2021.

Tires, which account for three in each 4 {dollars} spent on aftermarket purchases, grew +4% in comparison with 2022 income, whereas automobile chemical compounds (15% of aftermarket income) have been up +6% and spare components up +10%.

This progress is pushed partially by an enhance in premium purchases throughout phases – however that’s not the one issue.

Over the final couple of years, we’ve seen polarization between worth and quantity progress, as the common value of things soared, pushed by worldwide high inflation and elevated prices in manufacture and supply. That hole is now closing as costs begin to stabilize, though at excessive ranges.

-

Automotive tire traits: growth shifting to rising economies

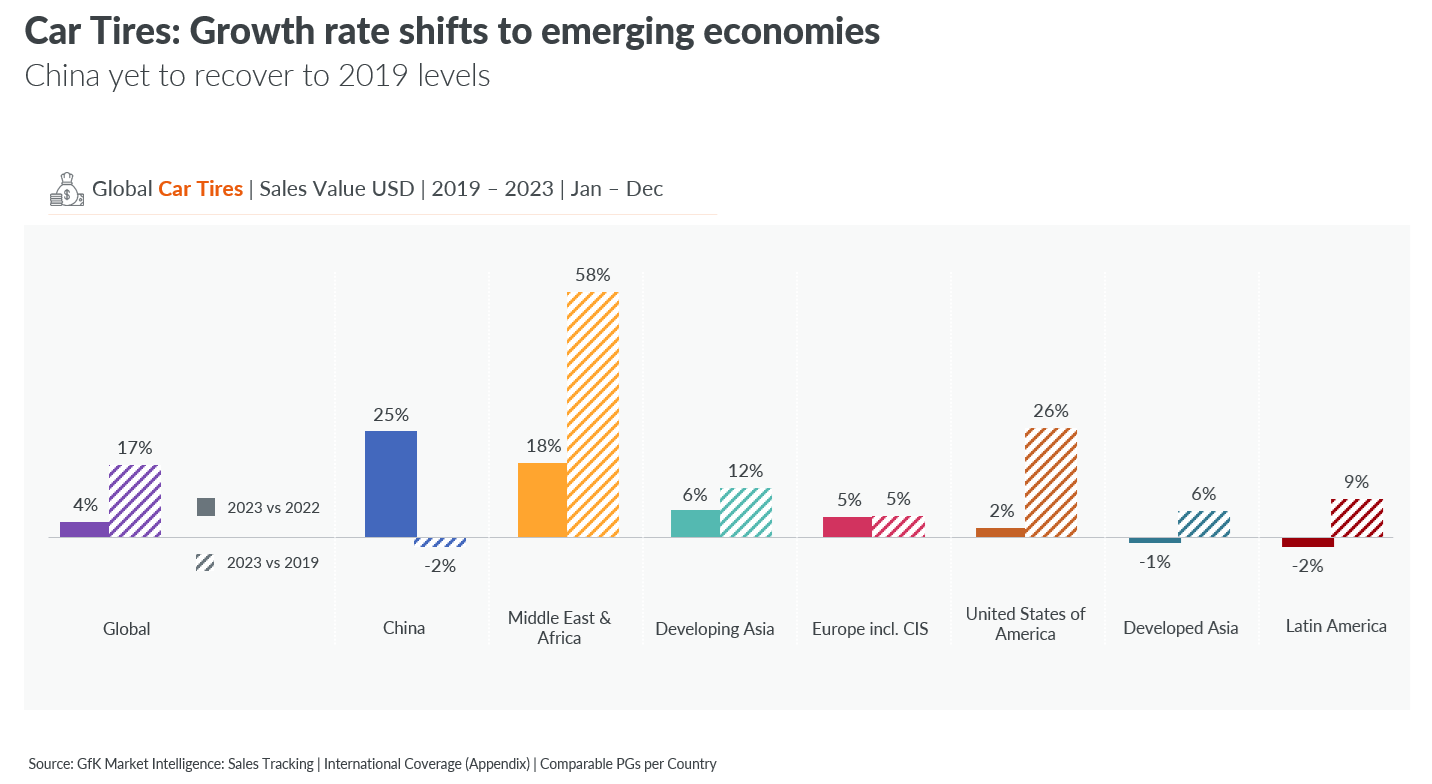

From a regional share perspective, Europe and US are the most important areas in income inside the automotive aftermarket trade. Taking a look at their gross sales of automobile tires final yr, each markets proceed to develop steadily, though at a slower price than earlier than, with 2023 delivering +5% progress in Europe and +2% in US.

The 2 quickest rising areas for automobile tires are China and the Center East and Africa. China recorded an wonderful +25% progress, yr on yr, with potential to develop nonetheless additional this yr, because the market has not but get bettered to its pre-pandemic 2019 ranges. The Center East & Africa area can be one of many excessive potential progress markets, continuing to register robust progress yr on yr.

Developing Asia was simply forward of Europe by way of progress – standing at +6%, whereas the Developed Asia and LATAM areas each confirmed a slight decline in income. These final two markets have robust headwinds, nonetheless, because of the excessive progress charges witnessed in 2022 setting difficult baselines.

Bigger manufacturers dropping share to funds manufacturers

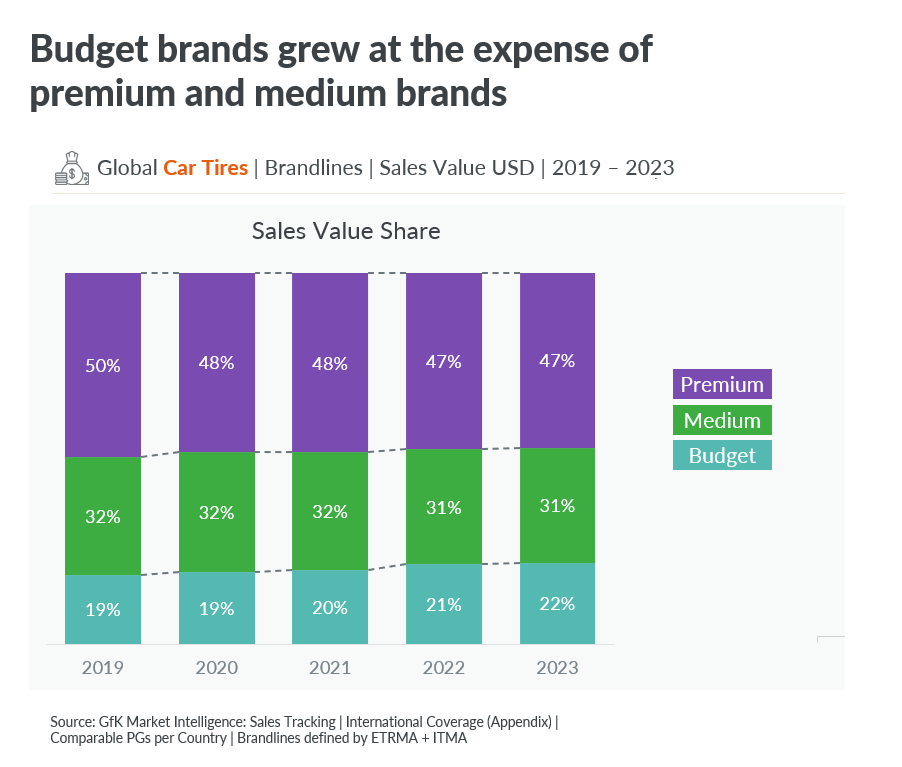

Globally, the unit share of automobile tires bought by smaller manufacturers has elevated from 29% to 33%. It’s truthful to imagine that that is pushed by customers shifting to decrease priced manufacturers as their family budgets have been squeezed final yr.

Given the numerous distinction within the value between premium, medium or funds model tires, funds choices stay a really economical alternative for the customers – particularly as the common price of funds model tires decreased very barely final yr, whereas medium and premium model tires rose.

This enlargement of funds manufacturers by way of market share is not confined to lower cost segments. Price range manufacturers are additionally providing increasingly more SKUs even in higher-finish tire segments, however at higher costs than the massive manufacturers. instance – tires with 18-inch-plus rims price an common 137 US {dollars} for a funds model, versus 237 {dollars} for a premium model.

Regional variations in progress of funds model tires

Globally, tire gross sales for funds manufacturers grew +6% final yr, whereas premium and medium manufacturers noticed round 3% progress. Nevertheless, there are regional variations on this pattern.

In Europe, medium manufacturers noticed the strongest progress, adopted by budget manufacturers, and with premium manufacturers showing significantly weaker efficiency. This circles again to the pattern we see of European drivers holding their automobiles longer and being much less inclined to spend cash on premium components as soon as they move 5 or 6 years previous.

LATAM, funds manufacturers grew an enormous +19%, whereas premium declined by –7% and medium manufacturers additionally noticed vital decline. This polarization in gross sales can be seen in the MEA and APAC areas, the place premium and funds each grew extra than medium manufacturers.

In the US market, nonetheless, we’re seeing clear premiumization, due to two key components. The primary is an financial system that is doing higher, and the second is the import restrictions positioned on (usually cheaper) Chinese language manufacturers on account of the geopolitical state of affairs between the 2 international locations.

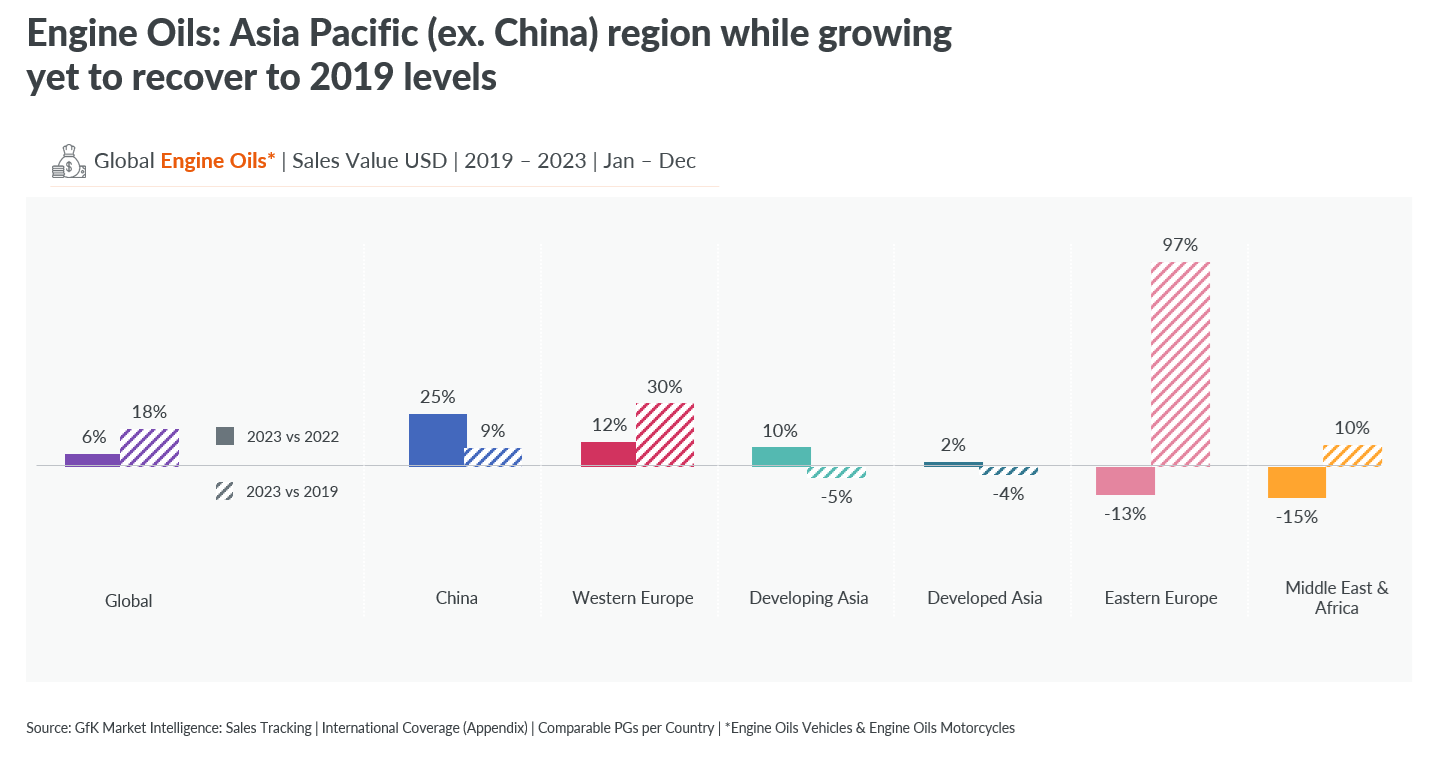

World income from gross sales of engine oils for each bikes and automobiles grew +6% final yr, led by China (+25%), Western Europe (+12%) and Creating Asia (+10%). Japanese Europe and Center East and Africa each confirmed declining income for engine oils.

In the Center East and Africa, the decline additionally represents the excessive baseline from final yr, in addition to the foreign money volatility (in native foreign money, progress there may be optimistic), and the ambition of some international locations on this area to have a lot greater deal with E-mobility.

dditional issue impacting these areas contains the native evolution of mobility, with cheaper choices corresponding to “trip hailing” being significantly widespread in areas corresponding to Southeast Asia and India.

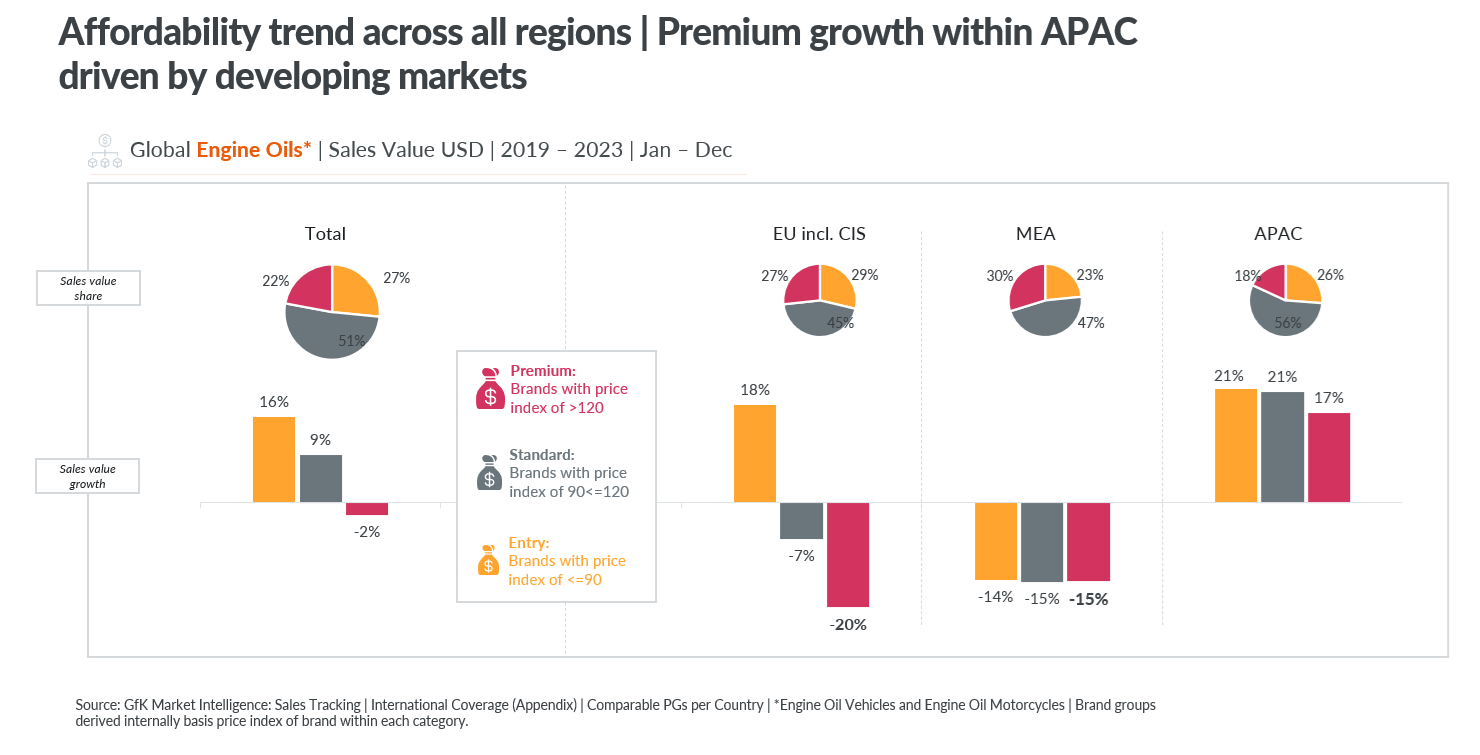

Price range shopping for carries by means of into engine oils.

Smaller manufacturers have significantly elevated their share of each income and quantity of engine oil gross sales, rising from 42% market worth in 2022 to 48% now. So, whereas the whole class gross sales income has elevated, those beneficial properties are principally being seen in the lengthy tail, or manufacturers with smaller market shares in comparison with the market leaders.

Globally, engine oils noticed a +16% enhance in the gross sales worth of entry manufacturers in comparison with +9% of normal manufacturers, whereas premium model gross sales declined by –2%. That affordability pattern is seen throughout all areas. with the entry–degree manufacturers doing significantly better than the remainder.

APAC is the one area displaying optimistic progress for engine oils, and this is pushed by the growing markets corresponding to Developed Asia, the place funds manufacturers have been the one part that grew.

Our forecast is that this pattern with continue by means of 2024, with customers looking for inexpensive choices for all upkeep merchandise – particularly as they hold their automobiles longer in markets corresponding to Europe and the USA. The chance for market leading manufacturers comes when customers buy a brand new automobile or face a vital subject with the present product they’ve used.

-

Automotive innovation outlook

For the automotive trade, like others, there are three forces that drive innovation: consumer demand, legislation / regulation, and manufacturer push.

During the last couple of years, now we have seen automotive innovation specializing in 6 themes:

- Safety

- Convenience

- Performance

- Design

- Sustainability

- Business fashions.

Wanting on the applied sciences that can affect or allow improvements within the automotive trade, AI continues to be the thrill phrase. Immersive know-how is enabling enhancements in client expertise and cholding the way in which customers work together with their automobiles. The Web of Issues, for instance, is being built-in into car know-how to drive transformation throughout design, manufacturing, operations and upkeep, whereas cloud computing is enabling automakers to remotely monitor car efficiency and predict upkeep wants.

Electrical autos additionally proceed to develop in each the patron and industrial spheres. In 2021, EVs accounted for 12% of all gross sales in 2021, rising to 21% in 2023 and are expected to hit 25% this yr. Three markets dominate these gross sales – China (over 50% of share of world gross sales final yr), Europe and the US – with different international locations tailing fairly far behind. From a client perspective, EVs are extra of an aspirational or standing image product, with the key attraction being much less about their eco-positioning and extra about the extent of tech included in these automobiles that allows them to do extra than simply drive. This focus means we’re seeing conventional tech manufacturers changing into more and more and influential within the automotive sector.

, then, might be linked, autonomous, shared and electrical. It would, nonetheless, take a very long time to succeed in that future, on account of challenges corresponding to market readiness, gradual implementation to turn out to be mainstream, and excessive manufacturing prices resulting in excessive promoting costs.

To optimize the success of their innovation technique, producers should preserve a laser-sharp monitoring of their viewerss, and align exactly with their evolving lifestyles, wants, aspirations and limitations.

Need to know extra?

{kind=link}