Cautious scrutiny of your retirement plans requires you to think about annuities to steadiness your funding portfolio. Annuities stay dependable funding autos to generate a assured revenue post-retirement. Meticulously deliberate annuities typically replicate month-to-month paychecks that mirror within the type of wage amidst rising rates of interest.

The place Will I Begin With My Annuities?

Properly, you could be in a dilemma about when to start out your annuities. Excellent timing ensures that you just profit from the market situations. In the event you plan to foretell the annuity charges sooner or later, it pays to start out investing on the proper time.

Including to all of the monetary dilemmas — the FED retains altering the rates of interest. So, what does growing rates of interest imply for annuities? We have now comprehensively lined the influence of climbing rates of interest for annuities on this article. Having this information will allow you to plan your investments and maximize your returns.

Various kinds of annuities within the US

Earlier than leaping to the rate of interest influence on annuities, first, allow us to be taught the varieties of annuities you’ll be able to spend money on the US.

1. Speedy annuities

Speedy annuities assure funds to the investor inside the first 12 months. It’s also possible to get personalized, assured revenue. As an illustration, you pay $200,000 as a single premium to your insurer. As per the settlement, the insurer pays you $5,000 per thirty days for a hard and fast interval in a while. The rates of interest and market situations decide the payout quantity.

Whereas deciding the kind of annuities, it is crucial to contemplate your age. In any other case, calculating your estimated necessities for retirement financial savings seems to be difficult. Buying instant annuities assist assure a lifetime payout, no matter your age.

Nonetheless, the investor can be buying and selling liquidity to warrant a hard and fast revenue. Throughout emergencies, you will not have entry to this fund.

The prime profit of buying instant annuities is that you just get to know precisely how a lot you’ll obtain after your retirement.

2. Deferred annuities

By way of deferred annuities, you’ll be able to obtain assured revenue sooner or later. This generally is a month-to-month influx of money or lump sum revenue. You want to pay month-to-month premiums or a lump sum quantity. Based mostly on the kind of funding you chose, the insurer will make investments the quantity persistently as per the contractual settlement. With deferred annuities, you’ll be able to develop the principal considerably. These investments additionally convey you the chance to avoid wasting taxes.

3. Fastened annuities

In the event you aren’t prepared to tackle larger threat, go for mounted facilities. As per the settlement, your insurer can pay you a hard and fast fee of curiosity in your funding, which is assured. You will obtain the payouts via an agreed time interval. As soon as the contract interval expires, you’ll be able to renew or annuitize your contract.

Apart from, one may get the invested {dollars} transferred into a special retirement account or annuity contract. Because the rate of interest is mounted, market volatility will not have an effect on your returns.

4. Variable annuities

A variable annuity refers to a contract the place the worth relies on how the underlying sub-accounts carry out. That is completely different from mounted annuities that provide a assured return. Nonetheless, you get to benefit from the scope of maximizing your returns by investing in a variable annuity. Nonetheless, these investments are usually riskier, as the worth of the sub-accounts may fall, similar to antagonistic market performances.

Variable annuities maintain the best revenue potential. These annuity contracts are tax-deferred, enabling the investor to channel funds into sub-contracts. That is just like your investments in a 401 (ok). These sub-accounts assist to keep up the expansion trajectory of your annuity.

At instances, these annuities may also help you beat inflation. The sub-accounts, similar to mutual funds, are topic to market efficiency and threat. Apart from, you will get an revenue rider or a dying profit rider with variable annuities.

What makes timing essential for investing in annuities?

Usually, the sale of annuities tends to shoot up with rising rates of interest. It is because folks can be curious about discovering a protected place to park their funds whereas incomes a good return. For higher returns throughout retirement days, beginning your annuities is essential when rates of interest stay excessive.

Then again, the gross sales of annuities dip with low-interest charges. Folks really feel the returns will not be too good throughout retirement. Naturally, they chorus from buying annuities when rates of interest are low.

Now that the rates of interest are hovering, individuals are eager to buy annuities. Even when your office retirement plan or 401(ok) is working dry, the revenue from the annuity will come in useful. Amidst a risky market and growing rates of interest, this is able to be a good time to buy your annuities.

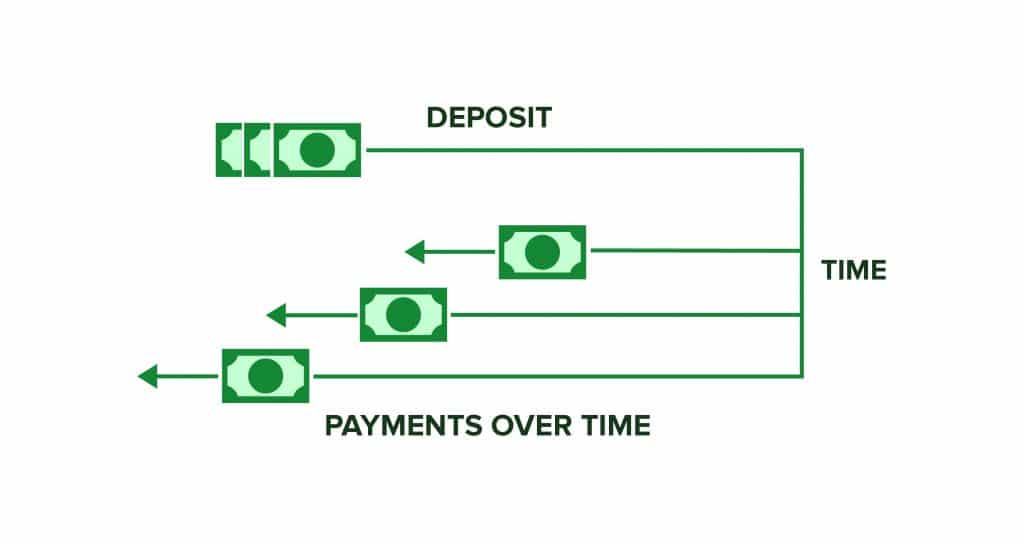

Annuities warrant a constant stream of month-to-month money influx

Annuities are designed to supply a constant month-to-month stream of revenue. That is just like your pensions and social safety. Whereas you’ll come throughout several types of annuities within the US monetary market, the core idea stays the identical. You pay premiums or make investments your funds with an insurer. The insurer, however, retains paying an everyday quantity of funds for the remainder of your life as per the settlement.

Since 2022, the common payouts from annuities have proven greater than a 13% increment for girls and 11% for males. This statistic relies on the information of a 65-year-old lady and a 70-year-old man who invested a $100,000 lump sum in annuities. As per CANNEX, the typical sum insurers provided on the finish of April 2022 was $616, whereas it was $553 at first of the 12 months. In 2023, the rates of interest have additional elevated, which might translate into larger annuity payouts.

Understanding the fundamentals of returns via annuities

Whether or not you go for a variable or mounted annuity for financial advantages, the issuer invests a large chunk of the property in fixed-income debt securities, bonds, index factors, or funding funds. Subsequently, the efficiency of debt securities largely determines the returns you achieve via annuities.

Whereas coping with bond issuers, the issuer of the annuity receives comparatively larger charges. The crediting fee, or the speed at which the annuity issuer pays to the annuity holder, is barely low. This distinction is known as “unfold.’

The commerce teams and regulators within the US often categorize the asset reporting for annuity merchandise and life insurance coverage collectively. In accordance with the Fed, annuity and life issuers maintain property value $9.8 trillion. This contains debt securities value $4.4 trillion. In 2021, life insurers boosted their bond holdings in debt securities by $141 billion.

In 2023, if life insurers make investments round $200 billion in bonds, it will lead to an increment of 1.9% within the new cash fee of the insurers. This may end up in an increment of $3.8 billion in a single 12 months by way of curiosity that the life insurers and their shoppers obtain.

Understanding the distribution of crediting charges and annuity unfold

- In accordance with S&P, listed annuity issuers assure that holders would obtain round a 3% to 4% common crediting fee.

- In December 2020, Moody’s Traders Service said 9 life insurance coverage firms within the US that had been encountering unfold compression issues assured charges between 4% and 5.5%.

- In 2021, American Fairness said that their mixture price of cash was 1.55%.

- Lincoln Monetary said that the typical rate of interest at which it credited annuity contract holders was 1.93%.

In June 2021, the Nationwide Affiliation of Insurance coverage Commissioners declared that the general common unfold of life insurers between the online funding portfolio yield and their promised fee to shoppers dropped from 1.8% in 2007 to 0.63% in 2020. The mixture funding unfold of American Fairness in 2021 was 2.18%, whereas it was 1.43% for Lincoln Monetary.

How do larger rates of interest translate into larger annuity payouts?

As an investor, it pays to know the components on which annuity payouts are calculated. Insurers take into account the shopper’s life expectancy and rates of interest as two of the prime determinants of payouts.

Amidst the pandemic, the Federal Reserve drastically diminished the rates of interest to spice up the US economic system. Nonetheless, throughout its latest conferences, the Central Financial institution has been compelled to extend the rates of interest on account of excessive inflation. The charges are additional anticipated to rise within the present 12 months.

Now, bonds proceed to be the cornerstone of the annuity portfolios of insurance coverage firms. With hovering rates of interest, they will generate a better return on new bonds. Naturally, they cross on the profit to their shoppers, and also you get to savor a better month-to-month money influx.

Once more, sure annuities, akin to multi-year assured annuities, serve like your financial savings account. On the finish of the time period, it’s possible you’ll determine to transform it right into a stream of normal month-to-month revenue.

The rate of interest for a five-year multi-year assured annuity on the finish of 2021 was 1.95%. Round Could 2022, it considerably rose to 2.9%. In 2023, the charges are additional more likely to enhance.

Naturally, traders are eager to buy annuities in order that they will profit from larger returns. Though the charges differ from one insurer to the following, they will nonetheless capitalize on the advantages. Earlier than investing, it pays to scrutinize the monetary energy score of the insurers.

Often, you’ll discover monetary companies like Moody’s, Fitch Rankings, A.M. Finest Firm, or S&P International Rankings attributing these scores. A excessive score implies that the insurer would be capable to generate extra revenue for you within the years to come back.

Why is the US annuity market rising?

Within the first quarter of 2022, mounted annuity gross sales within the US had been recorded at $35.2 million. This marks a 14% Y-o-Y progress. Presently, the entire annuity gross sales had been up by 4%, at $63.6 million. By the tip of 2022, the worth was $310.6 billion, up by 22% in comparison with 2021.

This increment in annuity gross sales corresponds with the rise of rates of interest. Evidently, the correlation explains that extra individuals are buying annuities because the rates of interest preserve growing. Their expectation of a better-guaranteed return within the coming years has been driving the US annuity market.

In 2023, the rates of interest are anticipated to rise additional, which might increase the purchasers’ expectations. It stays to be seen what awaits the market within the remaining quarters of 2023.

Why do you have to purchase mounted annuities with rates of interest climbing?

Because the rates of interest preserve rising, Individuals are bracing to speculate extra in annuities. Let’s consider the influence of accelerating rates of interest on debtors and traders.

In case you’re borrowing cash, this would not be a good time as you’ll find yourself paying extra on curiosity. As an illustration, householders must pay larger on their mortgages all through their tenure.

Now, if you’re having fun with a money influx via an instrument influenced by mortgaged charges, you’ll be on the gaining finish. To reap the benefits of the market situations, it will be a logical resolution to spend money on a hard and fast annuity. Because the rates of interest are growing, you’ll be able to lock the deal at a excessive fee all through the time period. Even when the Federal Reserve cuts the rate of interest after a number of months, the present fee can be relevant to you.

Insurance coverage firms within the US problem these annuities. The curiosity that these insurers earn via their pursuits determines the pay to their shoppers. Subsequently, a better rate of interest would translate into larger fee for you throughout the contract’s dispersal interval.

Let’s take a case that will help you perceive the situations higher. In case a 70-year-old lady invested $1 million as a premium to buy a life-only revenue annuity on twenty first December 2021, the annuity fee can be round $67,204. Nonetheless, the identical product might have fetched her $71,926 had she invested the identical quantity on twenty second March 2022. The distinction in fee is 7%, which may be even larger because the charges preserve growing in 2023.

Endnote

Annuities proceed to be a core share of a well-balanced funding portfolio. In case you are planning your retirement financial savings, it pays to contemplate the returns via annuities. Now that you understand why timing issues whereas beginning your annuities, this is able to be a good time to speculate.

With the rates of interest rising, annuity patrons can lock the speed and revel in assured returns after the tenure. Apart from, the Federal Reserve is more likely to additional increase the rates of interest in 2023. Even if you happen to accept a variable annuity, the climbing rates of interest promise superior returns.

The put up What Climbing Curiosity Charges Imply for Annuities? appeared first on Due.

{kind=link}