You are sensible, however beginning a small enterprise would not make you a finance professional. Accounting 101 is essential due to the money and time it will probably prevent sooner or later.

It would not matter in the event you love crunching numbers or take into account your self the extra artistic sort. Entrepreneurs have to pay attention to the monetary well being of their companies.

We wrote this information to ease you into the world of enterprise accounting. By the top, you’ll really feel able to sort out your individual enterprise’s accounting (or discover somebody who may help).

Preserve studying or use the chapter hyperlinks beneath to leap to the part you are on the lookout for.

What’s enterprise accounting?

Accounting is the method of systematically recording, analyzing, and deciphering what you are promoting’s monetary info. Enterprise house owners use accounting to trace their monetary operations, meet authorized obligations, and reinforce enterprise choices.

Accounting is a crucial a part of working a enterprise. It’s a activity you’ll both want to know or outsource — or each. Let’s ease into the subject with Accounting 101.

Accounting 101

Accounting is one thing that most individuals have heard about at work, on TV, or on-line. However that does not imply you actually get the fundamentals of accounting.

Like many careers, accounting is a mixture of tactical and analytical duties. And it isn’t simply recording transactions or doing taxes. Accounting is considering what your monetary data will imply to regulators, businesses, and tax collectors.

For those who’re answerable for accounting, it isn’t simply numbers and receipts. It is a means of gathering and reporting monetary info. You may use these experiences to speak the money flows, monetary place, and efficiency of what you are promoting.

Understanding accounting usually begins with studying primary phrases and rules. These may help you be taught the inspiration of accounting. Then, it is about studying how one can apply these practices.

However earlier than we dig into these concepts, let’s speak about what day-to-day work seems like for an accountant.

What do accountants do each day?

Accountants oversee the monetary data for a enterprise and ensure the info is appropriate. Then, they use this information to create budgets, monetary paperwork, and experiences.

Examples of this would possibly embrace a money movement assertion for operations or an revenue assertion for an upcoming board assembly.

Additionally they attend conferences to supply recommendation or look into authorized points. Different widespread actions embrace:

- Gathering new monetary information

- Reviewing or updating previous data

- Gathering proof for audits and different authorized proceedings

- Computing taxes

- Checking on compliance with related legal guidelines

- Ensuring tax funds are on time

- Forecasting and risk-assessment

Accounting Expertise

Accountants cannot simply be good with numbers. There are a lot of different technical and mushy expertise that this position makes use of every day to verify a enterprise is financially wholesome.

Vital expertise embrace:

- Listening

- Time administration

- Group

- Crucial pondering

These assist accountants collect info from stakeholders and talk their findings. Data of how the enterprise works can be important to contextualize monetary information.

Whereas math expertise are useful, information and programs evaluation are keys to success on this position. An accountant usually performs the position of investigator. Because of this curiosity and deductive reasoning expertise are additionally helpful.

For those who do not feel like these expertise are your strongest areas and also you run a enterprise, chances are you’ll need to hunt down assist to handle your accounting.

Accounting vs. Bookkeeping

These two would possibly sound the identical in the event you’re new to enterprise finance, however they’re very totally different.

To maintain it easy, bookkeeping is a tactical position, whereas accounting is extra strategic.

Bookkeepers document and set up monetary information for a enterprise.

Accountants analyze and advise enterprise leaders about what to do with that information. They provide insights on taxes, authorized issues, and progress. They put together experiences and audits to speak and current monetary information. These insights assist companies put together for surprising shifts that occur as a enterprise grows.

So, an accountant generally is a bookkeeper, however not all bookkeepers are accountants.

Primary Accounting For Your Enterprise: What You Must Know

Many small enterprise house owners do a mixture of bookkeeping and accounting.

For those who run a enterprise by yourself, chances are you’ll do some or all the following duties:

- Opening a checking account

- Monitoring revenue, bills, belongings, liabilities, and fairness

- Getting ready monetary statements

- Growing a system for bookkeeping

- Making a payroll system

- Determining tax laws and funds

Typically a enterprise will do that analysis and work as a part of an preliminary marketing strategy. Different occasions they find out about these necessities a bit bit at a time because the enterprise grows.

Accounting Automation

In keeping with Statista, 64% of small companies use accounting software program for his or her funds. One other 43% use software program for his or her taxes. Automated accounting software program consists of instruments like QuickBooks, Xero, and different in style accounting functions.

These instruments are how most small companies handle their accounting. Automation instruments save companies and accountants time by limiting the period of time they spend on information entry. This provides them extra time to research information to enhance the enterprise.

Most accounting software program is so fast and easy to make use of that it may be tempting to skip studying accounting phrases and rules. However this know-how makes it simpler to know a fancy audit or to search out errors in automated information.

Accounting Fundamentals

No matter the way you handle what you are promoting accounting, it is sensible to know accounting fundamentals. For those who can learn and put together these primary paperwork, you will perceive what you are promoting’s efficiency and monetary well being — in consequence, you will have higher management of your organization and monetary choices.

Listed below are the paperwork and calculations we suggest choosing up, even in the event you work with an expert, consulting company, or have employed a licensed public accountant (CPA). They supply helpful snapshots and measures of what you are promoting efficiency.

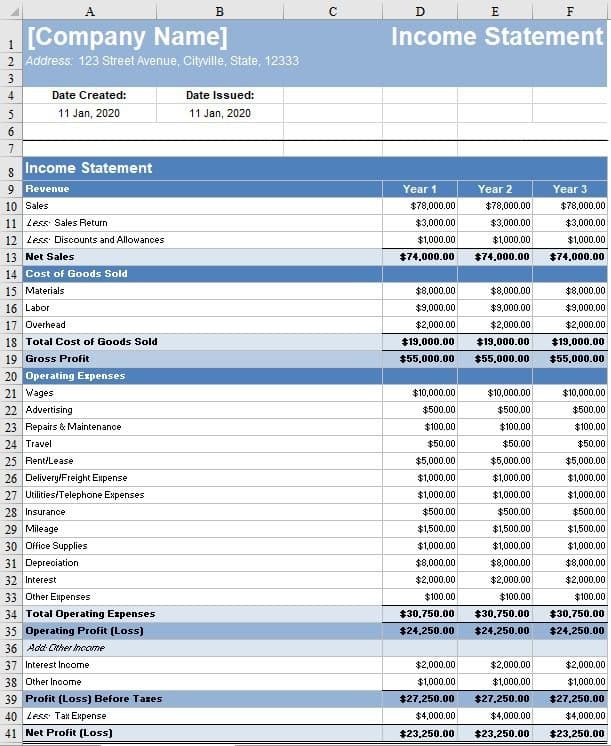

1. Revenue Assertion

An revenue assertion reveals your organization’s profitability and tells you ways a lot cash what you are promoting has made or misplaced

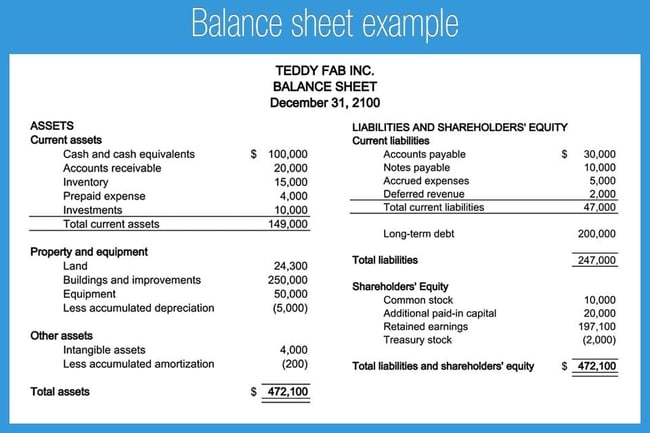

2. Stability Sheet

A stability sheet is a snapshot of what you are promoting’s monetary standing at a single cut-off date. A stability sheet can even present you what you are promoting’s retained earnings, which is the quantity of revenue that you just’ve reinvested in what you are promoting (relatively than being distributed to shareholders).

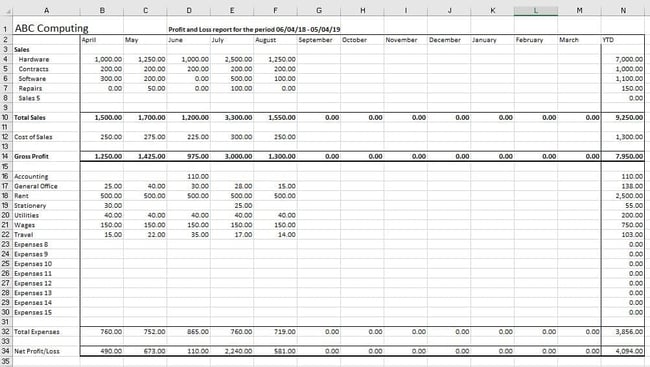

3. Revenue and Loss (P&L) Assertion

A revenue and loss (P&L) assertion is a snapshot of what you are promoting’s revenue and bills throughout a given time interval (like quarterly, month-to-month, or yearly). This calculation can even be mirrored on what you are promoting’s Schedule C tax doc.

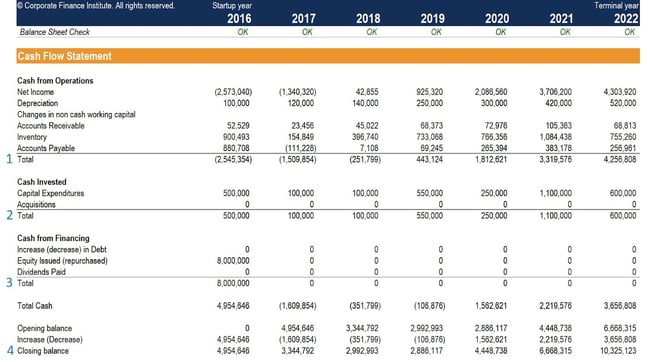

4. Money Move Assertion

A money movement assertion analyzes what you are promoting’s working, financing, and investing actions to indicate how and the place you’re receiving and spending cash.

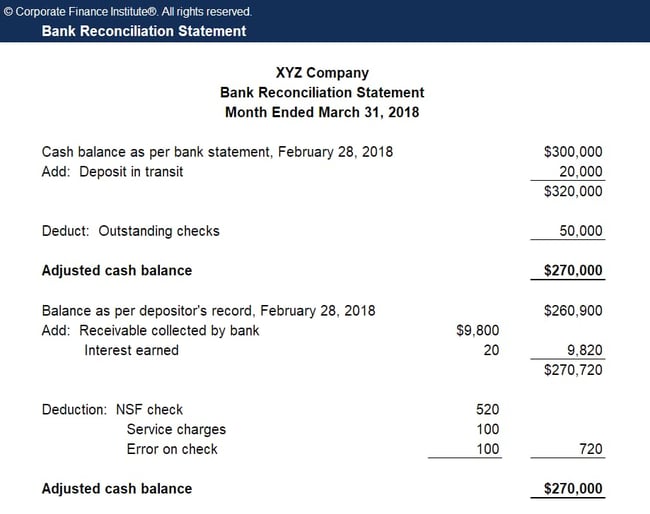

5. Financial institution Reconciliation

A financial institution reconciliation compares your money expenditures along with your general financial institution statements and helps preserve what you are promoting data constant. (That is the method of reconciling your e-book stability to your financial institution stability of money.)

Primary Accounting Phrases

These 15 phrases will create the inspiration on which you’ll construct your information of enterprise accounting. Whereas a few of these phrases may not apply to what you are promoting proper now, it’s vital to develop a holistic understanding of the topic in case you develop or transfer into one other sort of enterprise.

1. Debits & Credit

To not be confused along with your private debit and bank cards, debits and credit are foundational accounting phrases to know.

A debit is a document of all cash anticipated to come back into an account. A credit score is a document of all cash anticipated to come back out of an account. Primarily, debits and credit observe the place the cash in what you are promoting is coming from, and the place it’s going.

Many companies function out of a money account – or a enterprise checking account that holds liquid belongings for the enterprise. When an organization pays for an expense out of pocket, the money account is credited, as a result of cash is shifting from the account to cowl the expense. This implies the expense is debited as a result of the funds credited from the money account are protecting the price of that expense.

Right here’s a easy visible that can assist you perceive the distinction between debits and credit:

| debits | Credit |

| Improve belongings | Lower belongings |

| Lower liabilities | Improve liabilities |

| Lower income | Improve income |

| Improve the stability of expense accounts | Lower the stability of expense accounts |

| Lower the stability of fairness accounts | Improve the stability of fairness accounts |

2. Accounts Receivable & Accounts Payable

Accounts receivable is cash that individuals owe you for items and providers. It’s thought-about an asset in your stability sheet. For instance, if a buyer fulfills their bill your organization’s accounts receivable quantity is lowered as a result of much less cash is now owed.

Accounts payable is cash that you just owe different individuals and is taken into account a legal responsibility in your stability sheet. For instance, let’s say your organization pays $5,000 in hire every month. Right here’s how that will be recorded in your monetary data earlier than that quantity is paid out.

| date | account | debit | credit score |

| 7/31/21 | Lease | 5000 | |

| 7/31/21 | Accounts Payable | 5000 |

As soon as that worth is paid, right here’s how that will be recorded in your organization’s monetary data:

| date | account | debit | credit score |

| 8/1/21 | Accounts Payable | 5000 | |

| 8/1/21 | Money Account | 5000 |

3. Accruals

Accruals are credit and money owed that you just’ve recorded however not but fulfilled. These might be gross sales you’ve accomplished however not but collected fee on or bills you’ve made however not but paid for.

(Why not wait to document the exercise till the fee is full? We’ll reply this query once we clarify the accrual accounting methodology later.)

4. Belongings

Belongings are every part that your organization owns — tangible and intangible. Your belongings may embrace money, instruments, property, copyrights, patents, and emblems.

5. Burn Fee

Your burn charge is how rapidly what you are promoting spends cash. It’s a vital part when calculating and managing your money movement.

To calculate your burn charge, merely choose a time interval (resembling 1 / 4 or a 12 months). Subtract your on-hand money quantity on the finish of that interval out of your on-hand money at the start, then divide that quantity by the variety of months within the interval (or by your chosen cadence).

6. Capital

Capital refers back to the cash it’s important to make investments or spend on rising what you are promoting. Generally known as “working capital,” capital refers to funds that may be accessed (like money within the financial institution) and don’t embrace belongings or liabilities.

7. Price of Items Offered

The price of items offered (COGS) or price of gross sales (COS) is the price of producing your product or delivering your service.

COGS or COS is the primary expense you’ll see in your revenue and loss (P&L) assertion and is a vital part when calculating what you are promoting’s gross margin. Lowering your COGS may help you improve revenue with out rising gross sales.

8. Depreciation

Depreciation refers back to the lower in your belongings’ values over time. It’s vital for tax functions, as bigger belongings that affect what you are promoting’s potential to make cash may be written off primarily based on their depreciation. (We’ll focus on bills and tax write-offs later on.)

9. Fairness

Fairness refers back to the amount of cash invested in a enterprise by its house owners. It’s also referred to as “proprietor’s fairness” and may embrace issues of non-monetary worth resembling time, vitality, and different assets. (Ever heard of “sweat fairness”?)

Fairness can be outlined because the distinction between what you are promoting’s belongings (what you personal) and liabilities (what you owe).

A enterprise with wholesome (optimistic) fairness is engaging to potential traders, lenders, and patrons. Buyers and analysts additionally take a look at what you are promoting’s EBITDA, which stands for earnings earlier than curiosity, taxes, depreciation, and amortization.

10. Bills

Bills embrace any purchases you make or cash you spend in an effort to generate income. Bills are additionally known as “the price of doing enterprise”.

There are 4 fundamental sorts of bills, though some bills fall into a couple of class.

- Fastened bills are constant bills, like hire or salaries. These bills aren’t usually affected by firm gross sales or market tendencies.

- Variable bills fluctuate with firm efficiency and manufacturing, like utilities and uncooked supplies.

- Accrued bills are single bills which have been recorded or reported however not but paid. (These would fall below accounts payable, as we mentioned above.)

- Working bills are crucial for a corporation to do enterprise and generate income, like hire, utilities, payroll, and utilities.

11. Fiscal Yr

A fiscal 12 months is the time interval an organization makes use of for accounting. The beginning and finish dates of your fiscal 12 months are decided by your organization; some coincide with the calendar 12 months, whereas others differ primarily based on when accountants can put together monetary statements.

12. Liabilities

Liabilities are every part that your organization owes within the lengthy or quick time period. Your liabilities may embrace a bank card stability, payroll, taxes, or a mortgage.

13. Revenue

In accounting phrases, revenue — or the “backside line” — is the distinction between your revenue, COGS, and bills (together with working, curiosity, and depreciation bills).

You (or what you are promoting) are taxed in your internet revenue, so it’s vital to proactively plan in your tax legal responsibility. Do that by staying on high of your internet revenue quantity, setting apart a few of your income in a separate financial savings account, or paying your estimated taxes each quarter (like employer withholding).

14. Income

Your income is the overall amount of cash you acquire in alternate in your items or providers earlier than any bills are taken out.

15. Gross Margin

Your gross margin (or gross revenue), which is your complete gross sales minus your COGS — this quantity signifies what you are promoting’s sustainability.

Once more, these phrases are merely an introduction to enterprise accounting. Nonetheless, they may show you how to higher perceive accounting rules — which we overview subsequent.

Accounting Rules

Accounting requirements assist be sure that traders aren’t influenced by inaccurate monetary statements. Accounting rules affirm that publicly-traded firms share their funds precisely and constantly.

The Typically Accepted Accounting Rules (GAAP) are a blueprint for accounting throughout sectors and industries within the U.S. The Monetary Accounting Requirements Board (FASB) established the GAAP to uphold high quality requirements for accounting actions.

By legislation, accountants representing all publicly traded firms should adjust to GAAP. Let’s break down these rules.

1. Precept of Regularity

The working accountant is compliant with GAAP guidelines and laws.

Why this accounting precept is vital:

This precept regulates how accounting works as a occupation. With out it, each firm would handle funds in its personal means. This may make it powerful to maintain enterprise dealings honest.

apply this precept:

Comply with all Monetary Accounting Requirements Board (FASB) laws.

2. Precept of Consistency

This precept states that the accountant has reported all info constantly all through the reporting course of. Underneath the precept of consistency, accountants should clearly state any adjustments in monetary information on monetary statements.

Why this accounting precept is vital:

It makes certain that you could examine monetary reporting throughout an organization. Say you are evaluating two departments, however they document the identical transactions in several methods. This may make it tough for stakeholders to check them.

apply this precept:

Create clear processes for recording transactions and occasions as quickly as you begin what you are promoting. After getting a set course of for documenting and reporting your funds, keep on with it.

3. Precept of Sincerity

The accountant offers an correct monetary image of the corporate.

Why this accounting precept is vital:

This can be a promise from the accountant that they don’t seem to be making an attempt to mislead anybody. This helps traders belief that the knowledge what you are promoting presents is correct.

It is also a dedication to presenting information within the fairest and most correct means potential.

apply this precept:

Keep your monetary data actually and precisely.

4. Precept of Permanence of Strategies

All monetary reporting strategies ought to be constant throughout time durations.

Why this accounting precept is vital:

That is one other precept of regularity and consistency. It makes it simpler to check monetary data.

apply this precept:

Clearly set up your each day bookkeeping operations. It is also a good suggestion to create processes in order that your reporting stays constant over time.

5. Precept of Non-Compensation

All monetary info, each adverse and optimistic, is disclosed precisely. The right reporting of monetary information ought to be carried out with no expectation of efficiency compensation.

Why this accounting precept is vital:

It says that accountants should not alter reporting. As a substitute, accountants should decide to reporting each good and dangerous efficiency.

This sounds easy, however accounting can affect each inside and exterior opinions. Due to this, many publicly-traded firms report each GAAP and non-GAAP revenue. Typically this further information may help the general public picture of an organization or make clear the worth of an organization’s investments.

apply this precept:

Create monetary experiences which might be clear and correct.

6. Precept of Prudence.

Monetary information ought to be offered primarily based on factual info, not hypothesis.

Why this accounting precept is vital:

It makes certain that monetary statements are a practical overview of revenues and liabilities. It reminds firms to not over or understate their monetary threat.

apply this precept:

Enterprise strikes quick, and lots of firms depend on in-progress tasks and revenue to fulfill targets. However even when this is applicable to what you are promoting, proceed to keep up correct and well timed data.

Normally, do not anticipate earnings, however put together for any potential losses.

7. Precept of Continuity

This precept states the idea that the corporate will proceed operations.

Why this accounting precept is vital:

That is one other precept that is about belief. It says to base your accounting on how the enterprise runs now, not the way you hope it’ll run sooner or later. Even when an organization plans to make massive adjustments sooner or later, that should not change its worth at present.

apply this precept:

As what you are promoting plans for and makes adjustments, keep a constant course of for monetary reporting and record-keeping.

8. Precept of Periodicity

All accounting entries ought to be reported throughout related time durations.

Why this accounting precept is vital:

That is one other information in your reporting timeline. It makes it simpler for stakeholders to know and examine efficiency as a result of it separates it into quick durations of time. It additionally makes it simpler for them to see what essentially the most present monetary info is.

apply this precept:

Report in your funds yearly, quarterly, and month-to-month. It is also a good suggestion to set your fiscal 12 months if you begin what you are promoting.

9. Precept of Materiality

Accountants ought to goal to offer full disclosure of all monetary and accounting information in monetary experiences.

Why this accounting precept is vital:

Your corporation can determine which transactions are “materials” and which aren’t. Enterprise firms will method what’s and isn’t “materials” otherwise than a small enterprise would. If one thing is not “materials” it is one thing the enterprise feels is just too small to say.

For those who restrict your accounting to materials transactions it can save you time for what you are promoting. On the similar time, you need to be sure that monetary info that is vital to stakeholders is straightforward to entry and overview. This idea comes up most frequently throughout an audit.

apply this precept:

You would possibly begin what you are promoting accounting recording each transaction. However as what you are promoting grows or circumstances change, chances are you’ll need to revisit the way in which you document and report small transactions.

10. Precept of Utmost Good Religion

In keeping with this precept, events ought to stay sincere in all transactions.

Why this accounting precept is vital:

This precept establishes belief. It reinforces that you’ll share vital info with stakeholders earlier than you enter right into a contract collectively. This provides every individual a full and clear image of what you are promoting earlier than they make an settlement.

apply this precept:

Be clear and share important particulars as you make agreements.

How To Do Accounting For Small Enterprise

- Open a enterprise checking account linked to all factors of sale.

- Itemize all bills by division.

- Adhere to all revenue, employment, and excise taxes.

- Arrange a payroll system.

- Determine the fitting fee gateway in your wants.

- Perceive the tax obligations in your sort of enterprise.

- Usually overview and consider your processes.

- Seek the advice of with an expert or CPA.

Accounting is a fancy self-discipline. However in the event you’re not an accountant your self, you don’t have to know every part about accounting — solely the practices and components that must do along with your monetary operations, authorized obligations, and enterprise choices.

Whether or not you’ve simply launched what you are promoting or are a startup veteran, the next part is vital. These eight steps will introduce you to the accounting course of (in the event you’re not but acquainted) and set you as much as scale what you are promoting in a sustainable means.

Word: That is merely an summary of the self-discipline of accounting. We suggest conducting extra analysis and probably hiring an expert accountant (which we’ll speak about beneath) to make sure you don’t miss any monetary or authorized obligations.

1. Open a enterprise checking account linked to all factors of sale.

On your first order of enterprise, determine the place to maintain your cash. This will differ primarily based on what you are promoting’s authorized construction. If what you are promoting is an LLC, Partnership, or Company, you might be required to have a separate enterprise checking account. For those who’re a Sole Proprietorship, you don’t must — however we nonetheless suggest it.

Having a separate checking account for what you are promoting revenue and bills will make your accounting simpler. You’ll solely have one account to observe for bookkeeping and tax functions, and your private revenue and bills gained’t get entangled with what you are promoting ones. Imagine me — solely having to take a look at one set of financial institution statements is a lifesaver throughout tax season.

Search for a financial institution that has a neighborhood department in addition to sturdy on-line banking. Additionally, make sure the financial institution can combine along with your point-of-sale (POS) system and different technological wants. Enterprise financial institution accounts usually cost greater than private accounts and sometimes have the next minimal stability. Verify these numbers earlier than committing to a financial institution and a enterprise account.

We suggest opening two accounts — one checking account and one financial savings account, the latter by which you’ll stash cash for taxes and unexpected bills. And bear in mind, earlier than you may open any enterprise accounts, it’s essential to have a registered enterprise identify.

Lastly, take into account opening a enterprise bank card. Not solely will this assist offset some upfront bills, however it’ll additionally contribute to what you are promoting’s general credit score. Additionally, Firms and LLCs are required to have a separate line of credit score exterior their private accounts.

2. Itemize all bills by division.

Increase your hand in the event you’ve heard anybody say, “Hey, I can write that off.” I heard my mother and father say that lots once I was youthful — they’re each entrepreneurs — and I had no thought what it meant.

It wasn’t till I began my very own enterprise in faculty that I got here to know tax deductions: they’re a beautiful but pesky good thing about proudly owning a enterprise.

Many enterprise bills are tax deductions — bills that deduct from what you owe in taxes. For instance, if I spent $500 to fly to and attend a advertising and marketing convention, that’s $500 much less I owe in taxes for that 12 months. The catch? So as to declare a deduction, it is advisable to preserve a document of that expense.

Traditionally, conserving, submitting, and reviewing paper receipts was a time-consuming activity. (My mother used to pay 10-year-old me to arrange receipts by date and spotlight the seller and complete quantity … now I perceive why.)

At this time’s entrepreneurs have it a lot simpler. Software program, apps, and cloud-based bookkeepers have made it a breeze to trace bills and never must preserve a whole bunch of receipts mendacity round. Take a look at options like Rydoo, Expensify, Zoho Expense, and Shoeboxed to assist handle your bills.

Now, let’s focus on the bills and supporting documentation you’ll be managing. Whereas we are able to’t cowl each potential deduction, listed below are a handful it is best to positively preserve a document of. (Why? As a result of they’re straightforward to combine up with private bills … and the IRS is aware of it.)

- Promoting and advertising and marketing bills, resembling paid social media advertisements, web site internet hosting charges, and enterprise playing cards

- Enterprise journey, resembling aircraft tickets, motels, and rental vehicles

- Dwelling workplace bills, resembling WiFi, tools, and cellphones

- Automobile-related bills, resembling mileage and gasoline

- Meals and leisure, resembling journeys to espresso retailers, cafes, or concert events (until you don’t attend these occasions … then they’d be thought-about Presents)

In case it is advisable to help these bills, we suggest that you just preserve the next paperwork. (Rule of thumb: When unsure, preserve every part.)

- Receipts (paper and digital)

- Financial institution and card statements

- Payments (for utilities, telephone, web, and so forth.)

- Canceled checks

- Invoices and paperwork displaying proof of fee

- Monetary statements out of your bookkeeper or bookkeeping software program

- Tax returns from earlier years

- Any W-2, W-4, W-9, and 1099-MISC kinds

One other widespread solution to handle your bills is by separating working bills from promoting, common, and administrative (SG&A) bills.

Working and SG&A Bills

Some firms determine to mix working (OPEX) and SG&A bills whereas some separate them (they are often mixed on an revenue assertion). Both choice is completely positive — it is about desire.

This is what it is advisable to learn about OPEX versus SG&A bills:

- Working bills embrace prices associated to your each day bills and are sometimes nearly all of a enterprise’s bills (which is why many firms select to mix these bills).

- OPEX aren’t included in COGS — they’re the prices concerned within the manufacturing of products and providers resembling hire, utilities, insurance coverage, stock prices, salaries or wages, property taxes, or enterprise journey.

- SG&A bills are incurred as each day enterprise ops and are included in revenue statements (below “bills”).

- SG&A bills aren’t included in COGS (since they’re not related to a selected product) and are not assigned to your manufacturing prices.

- If separated from OPEX, SG&A covers components like accounting and authorized bills, advertisements and promotional supplies, advertising and marketing and gross sales bills, utilities and provides that are not associated to manufacturing, and company overhead (if there are government assistants and company officers).

3. Adhere to all revenue, employment, and excise taxes.

Ah. If solely bookkeeping meant hoarding the paperbacks I overbuy from my native bookstore — I’d be actually good at that.

Sadly, bookkeeping isn’t all the time as enjoyable. It’s one other vital account time period that refers back to the day-to-day recording, categorizing, and reconciling of transactions. Mainly, bookkeeping retains you from spending and earning profits with out monitoring it.

Bookkeeping is an ongoing activity. Technically, you need to be doing it each day, however everyone knows life can get in the way in which. Ideally, it is best to full your bookkeeping each month so you may preserve a thumb on the heartbeat of your revenue, bills, and general enterprise efficiency.

Earlier than we dive into how to do your bookkeeping, let’s cowl the two fundamental bookkeeping strategies.

Money Technique

The money methodology acknowledges income and bills on the day they’re truly acquired or paid. This methodology is the only for small companies as a result of it doesn’t require you to trace payables or receivables and displays whether or not or not your cash is definitely in your account.

Accrual Technique

The accrual methodology acknowledges income and bills on the day the transaction takes place, no matter whether or not or not it’s been acquired or paid. This methodology is extra generally used because it extra precisely depicts the efficiency of a enterprise over time.

The one factor it doesn’t present is money movement — a enterprise can look worthwhile however have zero {dollars} within the financial institution. If a enterprise’s annual income exceeds $5 million, it’s required to make use of the accrual methodology.

Now, let’s speak about how you are able to do your bookkeeping.

4. Arrange a payroll system.

Do you propose on hiring workers or contractors? Maybe you’re managing by yourself for now however are contemplating increasing sooner or later. Regardless, you’ll want to know and safe a payroll system.

Payroll is one other tedious but required a part of accounting. Fortunately, there’s loads of software program that may show you how to. (Hallelujah for modern-day expertise, proper? 🙌🏼) Take a look at options like Gusto, Zenefits, and Intuit Quickbooks Payroll.

Staff and impartial contractors are categorised otherwise and provides what you are promoting totally different tax deductions. Right here’s how you can deal with each.

Payroll For Staff

You possibly can deduct worker wages (salaries and fee bonuses), worker schooling bills, and worker advantages (accident and well being plans, adoption help, life insurance coverage, and extra) out of your taxes.

You may also deduct payroll taxes, that are employment taxes paid on behalf of your workers (like Social Safety and Medicare in addition to federal and state unemployment taxes).

Staff ought to submit a W-4 kind so you understand how a lot tax to withhold. In alternate, it is best to present workers with a W-2 kind, which summarizes their yearly gross pay. They use this to pay private taxes.

Payroll For Impartial Contractors

Impartial contractors embrace freelancers, consultants, and different outsourced specialists that aren’t formally employed by what you are promoting. With contractors, you don’t pay advantages or withhold taxes on their behalf.

Due to that, contractors ought to submit a W-9 kind so you might have their enterprise info (resembling their SSN or EIN), and it is best to present a 1099-MISC kind in alternate (in the event you pay them greater than $600 per 12 months).

A 1099 kind tells the federal government how a lot you spent for his or her providers — so you may write this quantity in your tax return, and to allow them to assume the tax burden on their return.

5. Determine the fitting fee gateway in your wants.

We’ve talked about your methodology of paying workers and contractors. Now, let’s speak about the way you’ll obtain cash in your items and providers. (This feels like extra enjoyable, huh?)

Your methodology of amassing cash is also known as your fee gateway. Whether or not you present freelance providers, arrange store at a neighborhood farmer’s market, or run a world e-commerce enterprise, you want a simple (and authorized) solution to acquire what you’ve earned.

Relying on the character of what you are promoting, the way you acquire cash will differ. Let’s go over some choices.

Fee Gateway For Service Supplier

As a contract author, I hardly ever work with purchasers in individual. The truth is, I’ve solely ever formally met certainly one of my purchasers — the remaining I work with purely over e mail. Due to that, I acquire most of my funds by an internet gateway.

PayPal is a well-liked alternative for amassing funds. You may also use software program like Wave, Xero, or Bench. Not solely are you able to bill purchasers by these packages, however you too can conduct bookkeeping, payroll, and different accounting duties. These cost charges, although, so take into account that when making your choice.

One other solution to acquire fee is thru cellular functions like Venmo or Sq. Money — simply you’ll want to ship an bill as proof of fee. Lastly, you may all the time acquire fee by way of test — it simply takes a bit longer than an internet switch. (Ship an bill with this methodology, too.)

Fee Gateway For Storefront Enterprise

Gathering cash in individual (at a storefront, market, and so forth.) can get expensive. Between tools, bank card charges, and dealing with bodily money, it may be a trouble. Fortunately, Sq. and PayPal make it straightforward to just accept card funds utilizing your smartphone or pill. These packages additionally ship your clients’ receipts, reconcile your transactions, and deal with returns if crucial.

For those who anticipate a excessive inflow of each day purchases, we suggest selecting a extra sturdy POS system and extra dependable tools (like a register and devoted card reader).

Each Sq. and PayPal provide this selection, too. With this selection, you’ll have to arrange a service provider account along with your financial institution. (This account acts as a center floor between your POS system and fundamental checking account.)

Fee Gateway For Ecommerce Enterprise

Ecommerce platforms like Shopify, BigCommerce, and WooCommerce usually present built-in fee gateways. These are all the time the best to undertake as they’re already built-in along with your web site. You possibly can additionally use third-party fee options like Stripe.

6. Perceive the tax obligations in your sort of enterprise.

Taxes are inescapable. Fortunately, they’re straightforward to arrange for. The easiest way to take action is to teach your self in your enterprise’s tax obligations, preserve correct data, and put aside income (or pay forward in quarterly taxes).

Paying taxes as a small enterprise is barely extra difficult than it’s as a person. The quantity and sort of taxes you file will rely on just a few issues: what you are promoting’s authorized construction, when you have workers (and what number of), and in the event you acquire gross sales tax.

This a part of accounting — tax obligation and assortment — is especially tedious. We extremely suggest that you just work with an expert to a minimum of guarantee what you are promoting is following the right procedures and legal guidelines.

7. Usually overview and consider your strategies.

Just like different processes and methods throughout what you are promoting, you will need to consistently overview and consider your accounting strategies. You need to all the time have a managed course of in place for what you are promoting accounting — as a result of, as you have realized all through the above sections, it is a fully vital facet of your organization’s general well being.

The frequency by which you overview and consider your strategies is sure to be distinctive to your particular enterprise. Nonetheless, it is regular (and really helpful) to audit your course of on the finish of each month, quarter, and 12 months. This fashion, nothing slips by the cracks or turns into an issue that is too massive to bounce again from.

If the character of what you are promoting is seasonal, you may tailor various factors just like the frequency of your analysis to this cycle. As an example, you would possibly require extra critiques of your accounting course of throughout excessive season, and fewer throughout slower months.

8. Think about an expert service or CPA.

As vital as it’s to know how enterprise accounting works, you don’t must do it alone. That’s the place skilled accounting providers and CPAs are available.

In case your finances permits, we extremely suggest hiring an expert to assist along with your accounting. Right here’s how one can go about doing so.

- Ask for a referral from a trusted pal or one other entrepreneur. For those who’re a part of any enterprise teams or networks, ask for suggestions there, too.

- Use the CPA listing.

- Use Yelp for native professionals.

Whomever you select, you’ll want to learn loads of critiques and testimonials about your potential accountant. Inquire about his or her expertise in your trade, charges, and providers, and be sure you’re comfy with how and the way usually you’ll talk along with your accountant earlier than you signal something. Set all expectations upfront.

Additionally, when you have the funds, hiring an in-house accountant is all the time an choice. This individual could be liable for what you are promoting’s accounting solely and be a contractor or full-time worker.

Study Enterprise Accounting to Develop Higher

Enterprise accounting would possibly look like a frightening mountain to climb, but it surely’s a journey nicely price it. Accounting helps you see your complete image of your organization and may affect vital enterprise and monetary choices.

From working towards calculations to understanding your organization’s tax obligations, studying the self-discipline of accounting can solely assist what you are promoting develop higher.

Even in the event you choose to make use of accounting software program or rent an expert, use the information we’ve reviewed on this information to know accounting fundamentals. Your corporation will thanks.

Editor’s be aware: This put up was initially printed in Could 2019 and has been up to date for comprehensiveness.

{kind=link}